Understanding life insurance can feel overwhelming, but it’s a crucial aspect of financial planning. This comprehensive guide dives deep into term life insurance, a popular and often misunderstood type of coverage. As stated on huythanh.org, “Choosing the right life insurance policy is a personal decision, but understanding the basics is the first step towards securing your family’s future.” Let’s explore the intricacies of term life insurance to help you make informed decisions.

Defining Term Life Insurance

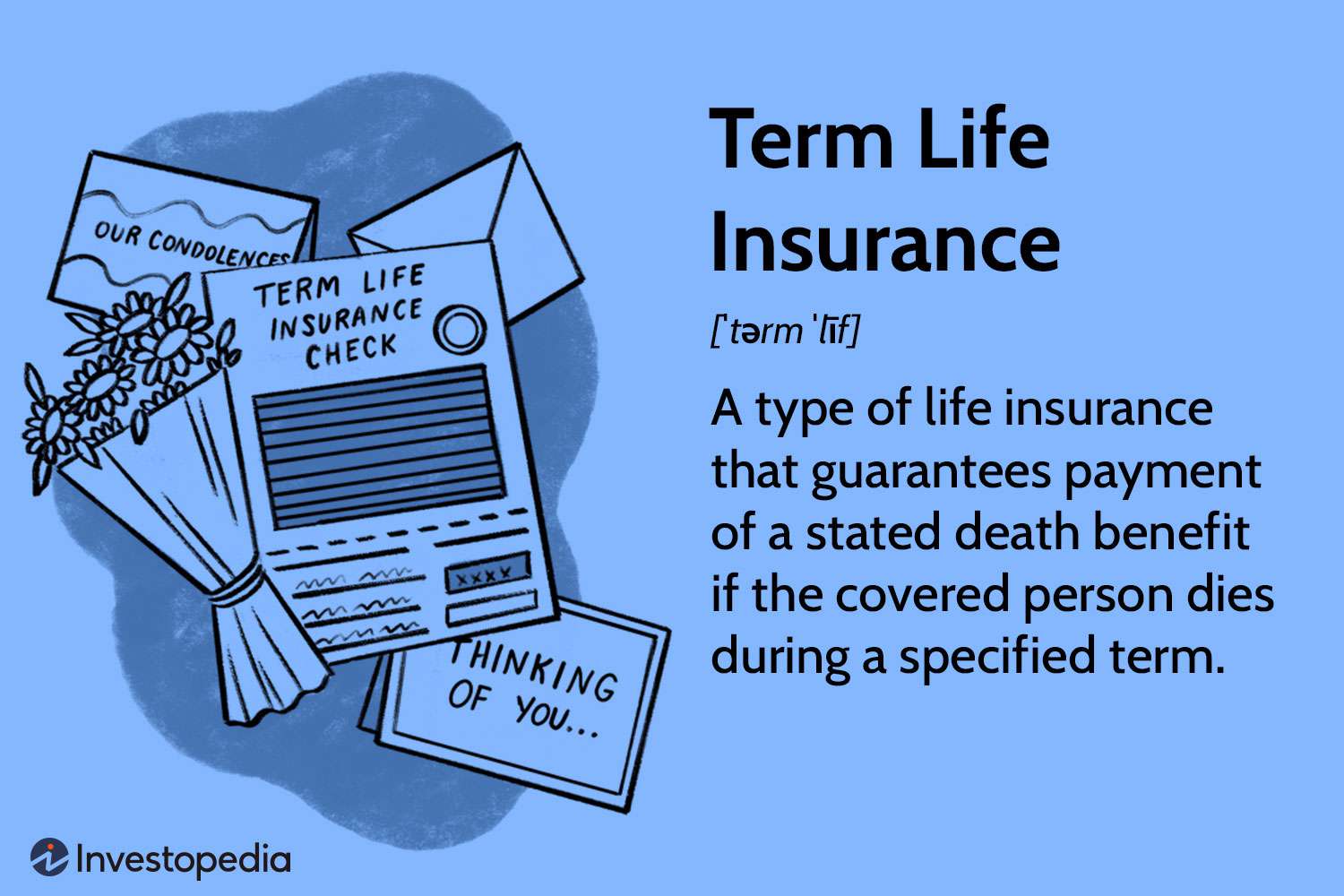

Term life insurance is a type of life insurance policy that provides coverage for a specific period, or “term.” Unlike whole life or universal life insurance, which offer lifelong coverage, term life insurance is temporary. If the insured person dies within the specified term, the beneficiaries receive the death benefit. If the insured person survives the term, the policy expires, and no further coverage is provided unless renewed.

Key Features of Term Life Insurance

Fixed Term: The policy covers a specific period, typically ranging from 10 to 30 years, although shorter and longer terms are available.

Level Premiums: Premiums remain constant throughout the policy term, making budgeting easier.

Death Benefit: A predetermined sum of money paid to the beneficiaries upon the death of the insured person during the term.

No Cash Value: Unlike permanent life insurance, term life insurance does not accumulate cash value. The policy solely provides death benefit protection.

Renewability and Convertibility: Many term life insurance policies offer options to renew the policy at the end of the term or convert it to a permanent policy.

How Term Life Insurance Works

The process of obtaining term life insurance is relatively straightforward. You apply to an insurance company, providing information about your health, lifestyle, and the desired coverage amount and term length. The insurance company assesses your risk and provides a quote. If you accept the offer, you begin paying premiums, and the coverage is active. Upon the death of the insured individual during the policy term, the beneficiaries submit a claim to the insurance company, providing necessary documentation. After verification, the death benefit is paid out.

Types of Term Life Insurance

Level Term Life Insurance: This is the most common type, offering a fixed death benefit and premium throughout the policy term.

Decreasing Term Life Insurance: The death benefit gradually decreases over time, while premiums remain constant. This type is often used to cover mortgages or other debts that decrease over time.

Return of Premium (ROP) Term Life Insurance: If the insured survives the policy term, the premiums paid are returned to the policyholder. This comes at a higher premium cost compared to standard term life insurance.

Increasing Term Life Insurance: The death benefit increases over time, usually at a fixed rate, while premiums also increase. This helps to maintain purchasing power against inflation.

Factors Affecting Term Life Insurance Premiums

Several factors influence the cost of term life insurance premiums. Understanding these factors can help you shop for the best policy.

Age: Premiums generally increase with age, as older individuals have a statistically higher risk of death.

Health: Pre-existing health conditions and current health status significantly impact premiums. Individuals with poor health typically pay higher premiums.

Gender: Traditionally, women have paid lower premiums than men, although this gap is narrowing.

Smoking Status: Smokers usually pay significantly higher premiums than non-smokers due to increased health risks.

Coverage Amount: A larger death benefit means higher premiums.

Policy Term: Longer policy terms generally lead to higher premiums per year, although the total cost may be less than shorter terms over the entire coverage period.

Insurance Company: Different insurance companies have varying underwriting practices and pricing models, leading to different premium costs.

Benefits of Term Life Insurance

Affordability: Term life insurance is generally more affordable than permanent life insurance, making it accessible to a wider range of individuals.

Simplicity: It’s easy to understand and purchase, with straightforward terms and conditions.

Flexibility: Many policies offer options for renewability and convertibility.

Targeted Coverage: It’s ideal for covering specific financial obligations, such as mortgages, debts, or childcare expenses, during a particular period.

Peace of Mind: It provides financial security for loved ones in case of unexpected death during the policy term.

Disadvantages of Term Life Insurance

Temporary Coverage: The coverage expires at the end of the term, leaving you without protection unless you renew or convert the policy. Renewal premiums will generally be significantly higher.

No Cash Value: No savings or investment component is built into the policy.

Potential for Increased Premiums at Renewal: Renewing a term life insurance policy often results in higher premiums, especially as you age.

Inability to Secure Coverage Later in Life: Securing a term life insurance policy becomes more difficult and expensive as you age.

When is Term Life Insurance a Good Choice?

Term life insurance is an excellent choice for several scenarios:

Young Families: Provides affordable coverage for families with young children, protecting against the financial burden of losing a primary income earner.

Mortgage Protection: Covers the outstanding mortgage balance in case of death, preventing financial hardship for surviving family members.

Debt Coverage: Protects against the financial strain of outstanding debts, such as student loans or credit card balances.

Temporary Financial Needs: Offers coverage for a specific period when financial protection is crucial, such as during a period of high debt or while raising young children.

Individuals on a Budget: Provides affordable life insurance coverage without the higher premiums associated with permanent policies.

Renewing and Converting Term Life Insurance

Many term life insurance policies offer the option to renew or convert the policy. Renewal allows you to extend the coverage beyond the initial term, typically at a higher premium. Conversion allows you to switch from a term life policy to a permanent life insurance policy, such as whole life or universal life, without undergoing a new medical examination. However, the premium for the converted policy will be significantly higher than the original term life policy premium.

Comparing Term Life Insurance to Other Types of Life Insurance

Term life insurance differs significantly from other types of life insurance, primarily in its temporary nature and lack of cash value. Whole life insurance offers lifelong coverage and accumulates cash value, but comes at a higher premium. Universal life insurance offers flexibility in premium payments and death benefit, but can be more complex to understand. Choosing the right type of life insurance depends on your individual needs and financial goals.

Finding the Right Term Life Insurance Policy

Shopping for term life insurance involves comparing quotes from multiple insurers, considering your specific needs and budget. Factors to consider include the desired death benefit, policy term, renewability and convertibility options, and the financial stability of the insurance company. Using online comparison tools and consulting with a financial advisor can aid in making an informed decision.

Conclusion

Understanding term life insurance is a critical step in securing your family’s financial future. By carefully weighing the advantages and disadvantages and considering your individual circumstances, you can choose a policy that offers the appropriate level of protection for your specific needs.